Because this is a question I get asked nearly every day, I´ve decided to make it easier to find the answer to this question.

Currently, this is who qualifies for a 100% mortgage:Anybody residing in the European Union, whose employment or pension income is derived from the European Union. Your net income must also be at least 2.5x higher than your total outgoings on loans and mortgages (both existing and applied for), eg if your income after tax is 2,500 euros per month, then your total loan and mortgage payments must not be higher than 1,000 euros per month. The property must be a repossession or distressed property from the bank offering the 100% loan.

In some cases the bank will allow you to include 70% of potential future rental income in your income calculation. They will use an independent valuer to assess this, eg if the valuer thinks the property has a potential rental income of 500 euros per month, then this could count as 350 euros income when they are assessing your eligibility for the mortgage.

Who qualifies for a 105% mortgage?Anyone who has been a permanent resident in Spain for some time, AND WHOSE INCOME (WHETHER EMPLOYMENT OR PENSION) IS DERIVED WITHIN SPAIN. This excludes Spanish residents drawing a pension from another country. Again, your net income must be at least 2.5x higher than your repayments on loans and mortgages.

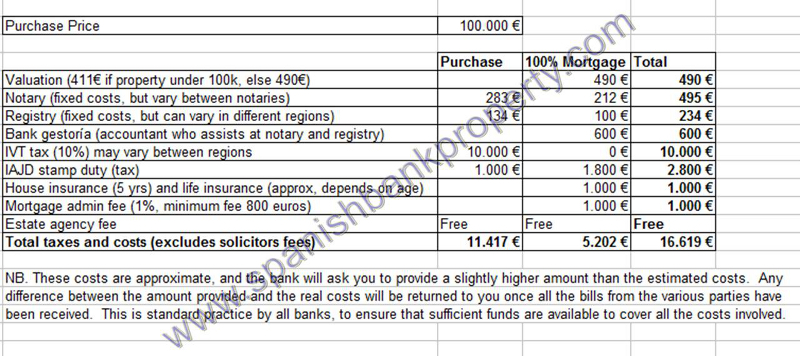

What are the taxes and costs involved?For clients taking advantage of this kind of mortgage, the taxes and costs are approximately 14% and taking a 100k mortgage on a 100k property as an example, this table shows how that 14% breaks down:

For non-residents, this 14% is the amount you have to provide from your own funds. Because 14% is equivalent to about one-seventh, you can calculate your maximum purchase price by multiplying your savings by 7. eg if your savings are equivalent to 20,000 euros, then you should be looking at properties with purchase prices of no more than 140,000 euros.

What is the maximum term?The difference between your age and 75, but no more than 35 years. eg if you are 30 the max term is 35 years, but if you are 50 the max term is 25 years.

Also please note that clients over 60 must present younger guarantors who can demonstrate capacity to repay the mortgage in their own right.

THEME SELECTOR

THEME SELECTOR